Detecting serially correlated errors and correcting inference using Newey-West standard errors.

Chapter purpose

Many economic datasets are collected over time. Examples include food prices, exchange rates, inflation, GDP, and stock prices. Unlike cross-sectional observations, time-series observations often exhibit persistence. What happens today is frequently related to what happened yesterday.

Regression analysis assumes that error terms are independent from one observation to the next. When this assumption is violated, the model suffers from autocorrelation.

In this chapter, we learn what autocorrelation is, why it occurs, how to detect it, and how to improve inference using Newey-West standard errors.

Applied question

Can monthly wheat prices be explained by a long-term trend?

Suppose we observe monthly wheat prices over several years.

Economic theory suggests that prices may gradually increase over time because of inflation, population growth, and rising production costs.

However, unexpected shocks rarely disappear immediately. If prices are unusually high this month, they may remain above average next month. This persistence often creates autocorrelation.

Economic background

Many economic variables exhibit momentum.

Examples include:

food prices

housing prices

exchange rates

inflation

agricultural commodity prices

A drought that increases wheat prices today may continue affecting prices for several months. Similarly, a recession that reduces consumer demand today may continue influencing economic activity next quarter.

As a result, regression errors often display patterns over time.

Key idea

The classical regression model assumes:

[ Cov(u_t,u_s)=0 ]

for all (t s).

This means that errors from different time periods are unrelated.

Autocorrelation occurs when errors are correlated across time:

[ Cov(u_t,u_{t-1}) ]

Positive autocorrelation is most common. In this case, positive errors tend to be followed by positive errors and negative errors tend to be followed by negative errors.

Simulating wheat price data

To illustrate autocorrelation, we create a synthetic monthly wheat price series. The price follows a trend, while shocks persist through time.

import numpy as npimport pandas as pdnp.random.seed(4107)n =120time = np.arange(n)errors = np.zeros(n)for t inrange(1, n): errors[t] =0.8* errors[t -1] + np.random.normal(0, 5)price =200+0.5* time + errorswheat_data = pd.DataFrame({"Month": time,"Price": price})wheat_data.head()

Month

Price

0

0

200.000000

1

1

204.705084

2

2

197.800607

3

3

195.408530

4

4

193.581992

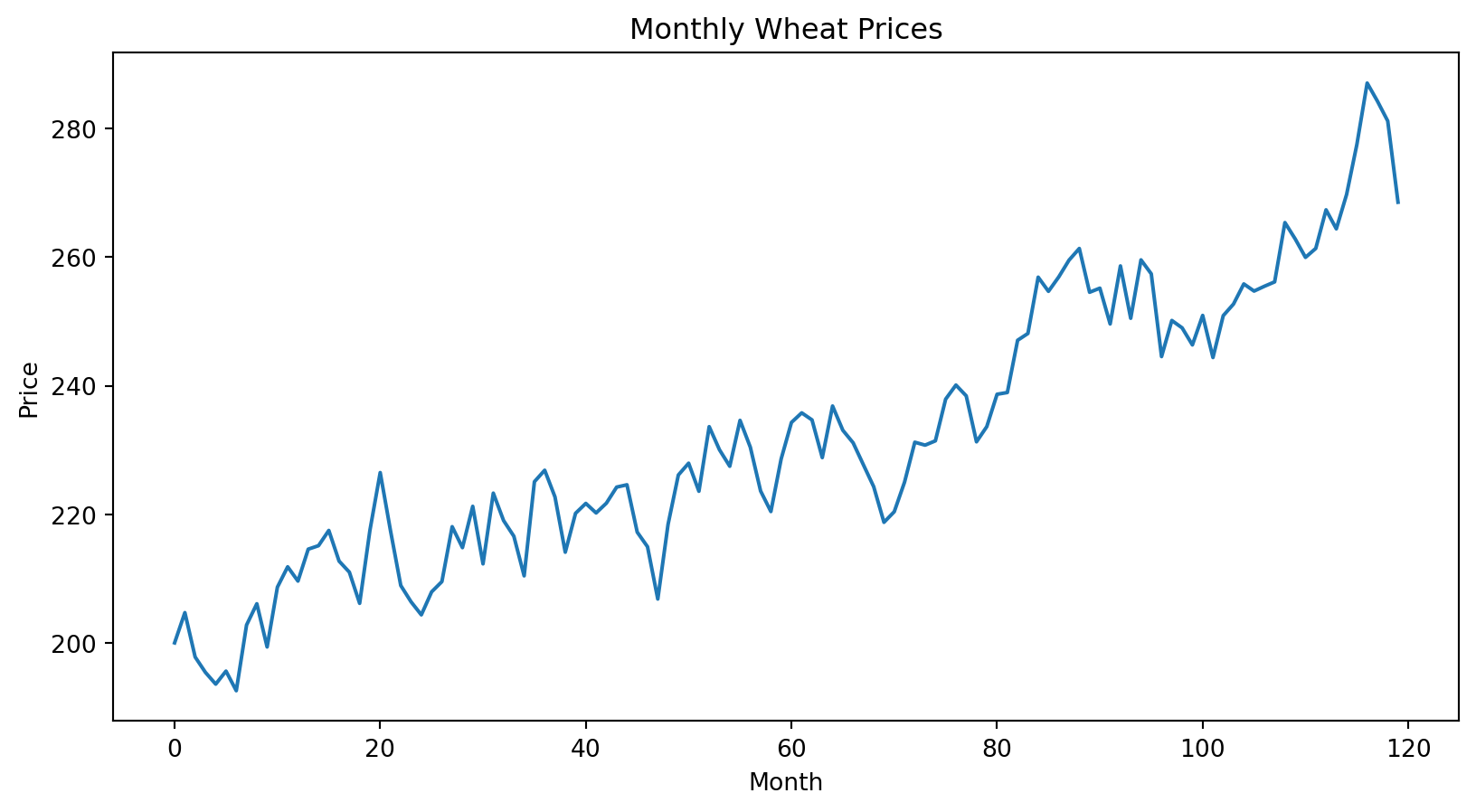

Visualizing the data

import matplotlib.pyplot as pltplt.figure(figsize=(10, 5))plt.plot( wheat_data["Month"], wheat_data["Price"])plt.xlabel("Month")plt.ylabel("Price")plt.title("Monthly Wheat Prices")plt.show()

Interpretation

The graph shows an upward trend. Notice that prices do not fluctuate randomly around the trend. Instead, periods of high prices tend to cluster together and periods of low prices tend to cluster together.

On average, wheat prices increase by approximately 0.52 units per month.

The coefficient measures the average trend. However, it does not tell us whether the residuals satisfy the assumptions of the regression model.

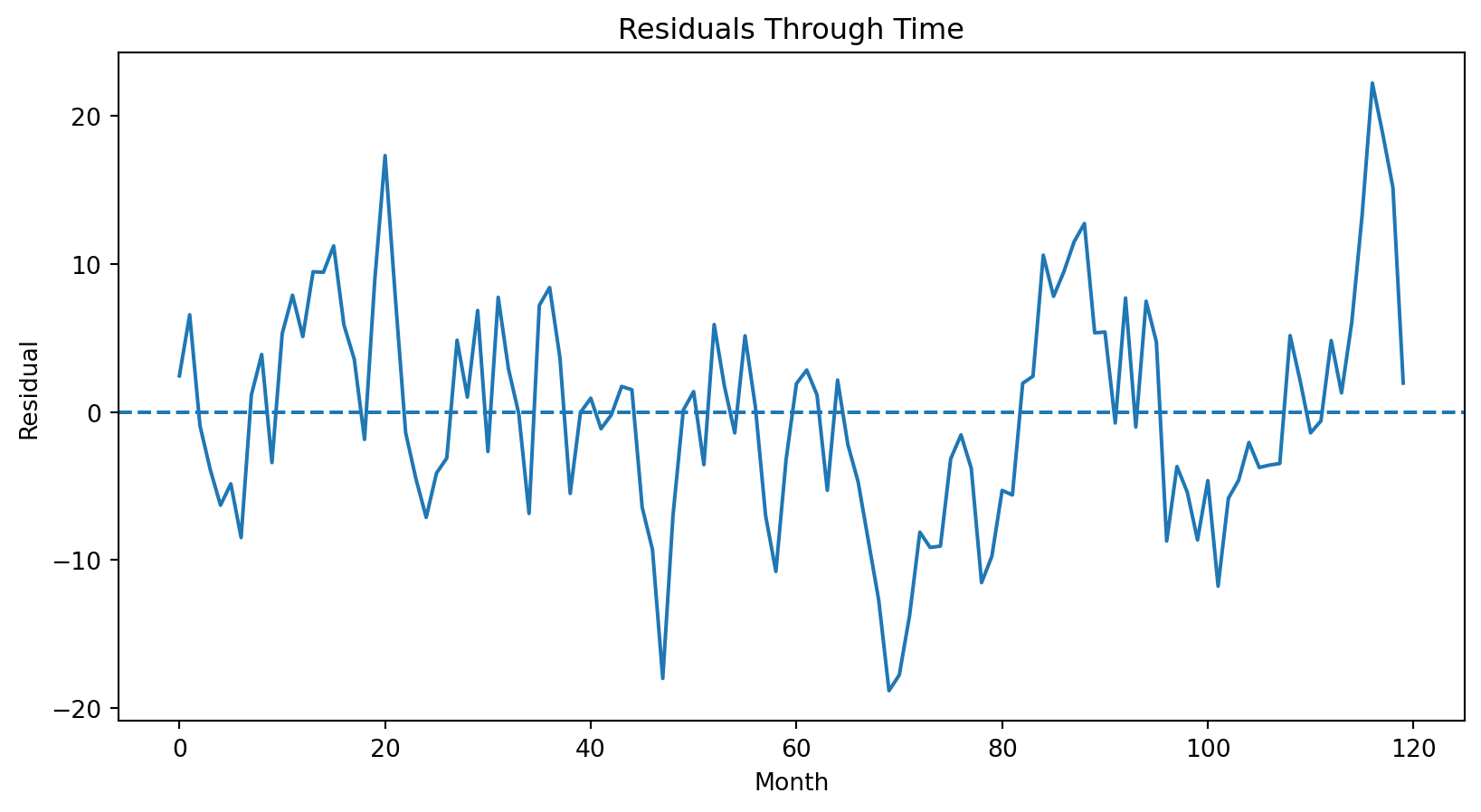

Residual time plot

The first diagnostic is a plot of residuals over time.

residuals = model.residplt.figure(figsize=(10, 5))plt.plot( wheat_data["Month"], residuals)plt.axhline( y=0, linestyle="--")plt.xlabel("Month")plt.ylabel("Residual")plt.title("Residuals Through Time")plt.show()

Interpretation

If residuals are independent, they should bounce randomly above and below zero. Instead, long runs of positive residuals and long runs of negative residuals appear.

This suggests autocorrelation.

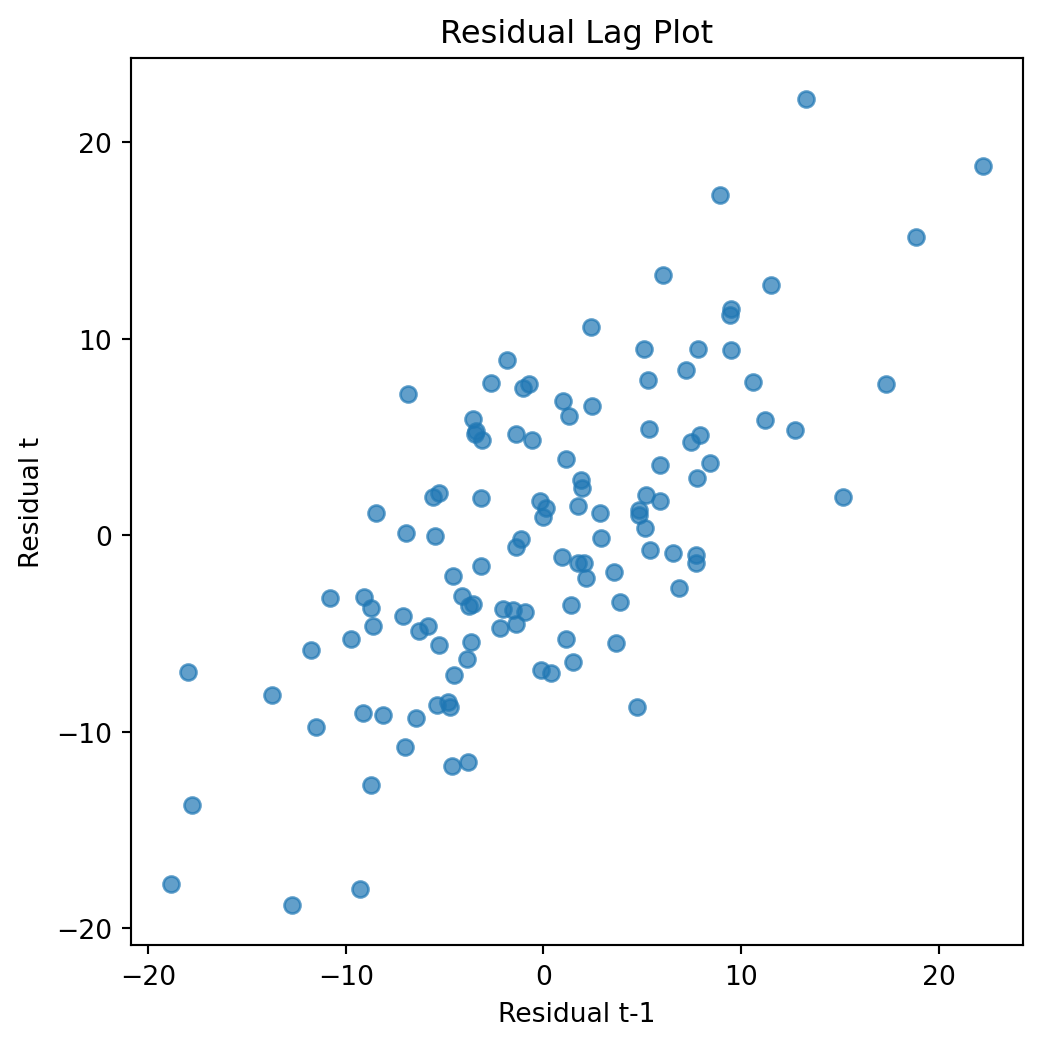

Residual lag plot

Another useful visualization compares each residual with the previous residual.

plt.figure(figsize=(6, 6))plt.scatter( residuals[:-1], residuals[1:], alpha=0.7)plt.xlabel("Residual t-1")plt.ylabel("Residual t")plt.title("Residual Lag Plot")plt.show()

Interpretation

If residuals are independent, the points should form a random cloud. A clear upward pattern indicates positive autocorrelation.

Large positive residuals tend to follow large positive residuals. Large negative residuals tend to follow large negative residuals.

The Durbin-Watson statistic

A commonly used diagnostic is the Durbin-Watson statistic.

from statsmodels.stats.stattools import durbin_watsondw = durbin_watson(model.resid)print(dw)

0.5856399966901465

Interpretation

The Durbin-Watson statistic ranges between 0 and 4.

Value

Interpretation

Around 2

No autocorrelation

Below 2

Positive autocorrelation

Above 2

Negative autocorrelation

In many economic applications, values substantially below 2 indicate positive autocorrelation.

Why autocorrelation matters

Autocorrelation creates several problems. The most important consequence is unreliable standard errors.

This can lead to:

confidence intervals that are too narrow

incorrect hypothesis tests

overstated statistical significance

excessive confidence in results

Just as heteroskedasticity affects inference, autocorrelation primarily affects how we evaluate uncertainty.

Newey-West standard errors

A common solution is to estimate heteroskedasticity and autocorrelation consistent standard errors. These are often called Newey-West standard errors.

OLS Regression Results

==============================================================================

Dep. Variable: Price R-squared: 0.879

Model: OLS Adj. R-squared: 0.878

Method: Least Squares F-statistic: 256.5

Date: Thu, 11 Jun 2026 Prob (F-statistic): 2.25e-31

Time: 06:54:24 Log-Likelihood: -411.15

No. Observations: 120 AIC: 826.3

Df Residuals: 118 BIC: 831.9

Df Model: 1

Covariance Type: HAC

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 197.5536 1.993 99.135 0.000 193.607 201.500

Month 0.5801 0.036 16.016 0.000 0.508 0.652

==============================================================================

Omnibus: 1.304 Durbin-Watson: 0.586

Prob(Omnibus): 0.521 Jarque-Bera (JB): 0.839

Skew: 0.144 Prob(JB): 0.657

Kurtosis: 3.291 Cond. No. 137.

==============================================================================

Notes:

[1] Standard Errors are heteroscedasticity and autocorrelation robust (HAC) using 4 lags and without small sample correction

Comparing standard errors

comparison = pd.DataFrame({"OLS Standard Error": model.bse,"Newey-West Standard Error": nw_model.bse})comparison

OLS Standard Error

Newey-West Standard Error

const

1.361885

1.992766

Month

0.019781

0.036217

Interpretation

The coefficient estimates remain unchanged. Only the estimated uncertainty changes.

Newey-West standard errors generally provide more reliable inference when residuals are correlated over time.

Why time-series data require extra care

Cross-sectional observations are often independent. Time-series observations are rarely independent.

Economic shocks frequently persist. Because of this persistence, economists routinely examine autocorrelation whenever they work with time-series data.

Ignoring autocorrelation can make a model appear more precise than it really is.

WarningCommon mistake

A high (R^2) does not imply independent residuals. A trend model can fit well and still suffer from strong autocorrelation.

Common mistakes

Mistake 1: Ignoring time order

Time-series observations should never be treated as randomly ordered observations. The sequence matters.

Mistake 2: Looking only at (R^2)

A model can have a high (R^2) and still suffer from severe autocorrelation.

Mistake 3: Assuming large samples solve the problem

Autocorrelation can remain important even in very large datasets.

Mistake 4: Reporting conventional standard errors

OLS standard errors may underestimate uncertainty when residuals are correlated.

Mistake 5: Ignoring residual diagnostics

Plots often reveal autocorrelation immediately. Always inspect residual patterns.

Key takeaways

Autocorrelation occurs when regression errors are correlated across time.

Time-series data frequently exhibit persistence.

Residual plots often reveal autocorrelation visually.

The Durbin-Watson statistic provides a useful diagnostic.

Autocorrelation primarily affects standard errors and inference.

Newey-West standard errors often improve reliability.

Economic time series require additional diagnostic checks.

Autocorrelation involves relationships among errors across time. In the next chapter, we examine multicollinearity, which occurs when explanatory variables contain similar information.